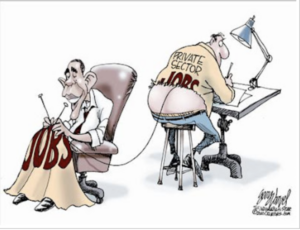

Crowding out by Russ Roberts on February 22, 2010 Tweet Cartoon by Gary Varvel. (HT: The New Seditionists) Share Tweet Share Email PrintComments