One sign of a seller trying to phish people for phools is the seller’s exaggeration of the size of the problem that the seller’s product allegedly will help the buyer to avoid. George Akerlof and Robert Shiller exaggerate the size of the problem that they claim to diagnose in Phishing for Phools. Consider:

Page xiii: “A fundamental fact of economic life has never made it into the economics textbooks. Most adults, even in rich countries, go to bed at night worried about how to pay the bills…. It is thus no coincidence that, as rich as we are in the United States, for example, relative to all previous history, most adults still go to bed worried about their bills…. No one wants to go to bed at night worried about the bills. Yet most people do.”

Page 9: “Chapter 1 shows why most consumers end the month, or the week, worrying about how to pay their bills, and quite frequently fail to do so.”

Page. 19: “Even in the current United States, where the vast majority of the population has a level of consumption unparalleled in human history, most people worry about how to make the ends meet.”

Page 188: Criticizing a (straightforward and indisputably correct) claim about the limits of the theory of consumer choice made in Greg Mankiw’s Principles of Economics textbook, Akerlof and Shiller write that “[t]his is good rhetoric, but you are not told that ‘the model’ fails to predict [financial advisor] Suze Orman’s worried clients, and the billions like them.”

Nowhere in their book, by the way, do Akerlof and Shiller supply data or references to data that support the claim (or the implication of the claim) that “most” Americans go to bed at night worried about how to pay their bills, or that “billions” (!) of people are suffering financial concerns of the sort that draw the advice of popular financial advisers such as Suze Orman. When such claims are accompanied by footnotes with citations to research, the research cited, if it doesn’t outright contradict, does not support Akerlof’s and Shiller’s clear implication that “most” Americans daily, or at least most of the time, suffer significant anxiety about their finances. See, for example, footnote 19 on page 182, which comes closest to supporting Akerlof’s and Shiller’s claim – but it’s still not very close at all. In this footnote Akerlof and Shiller cite a survey that finds (as Akerlof and Shiller summarize it) that

[n]early three-quarters (72 percent) of adults report feeling stressed about money at least some of the time and nearly one-quarter say that they experience extreme stress about money (22 percent rate their stress about money during the past month as an 8, 9, or 10 on a 10-point scale.

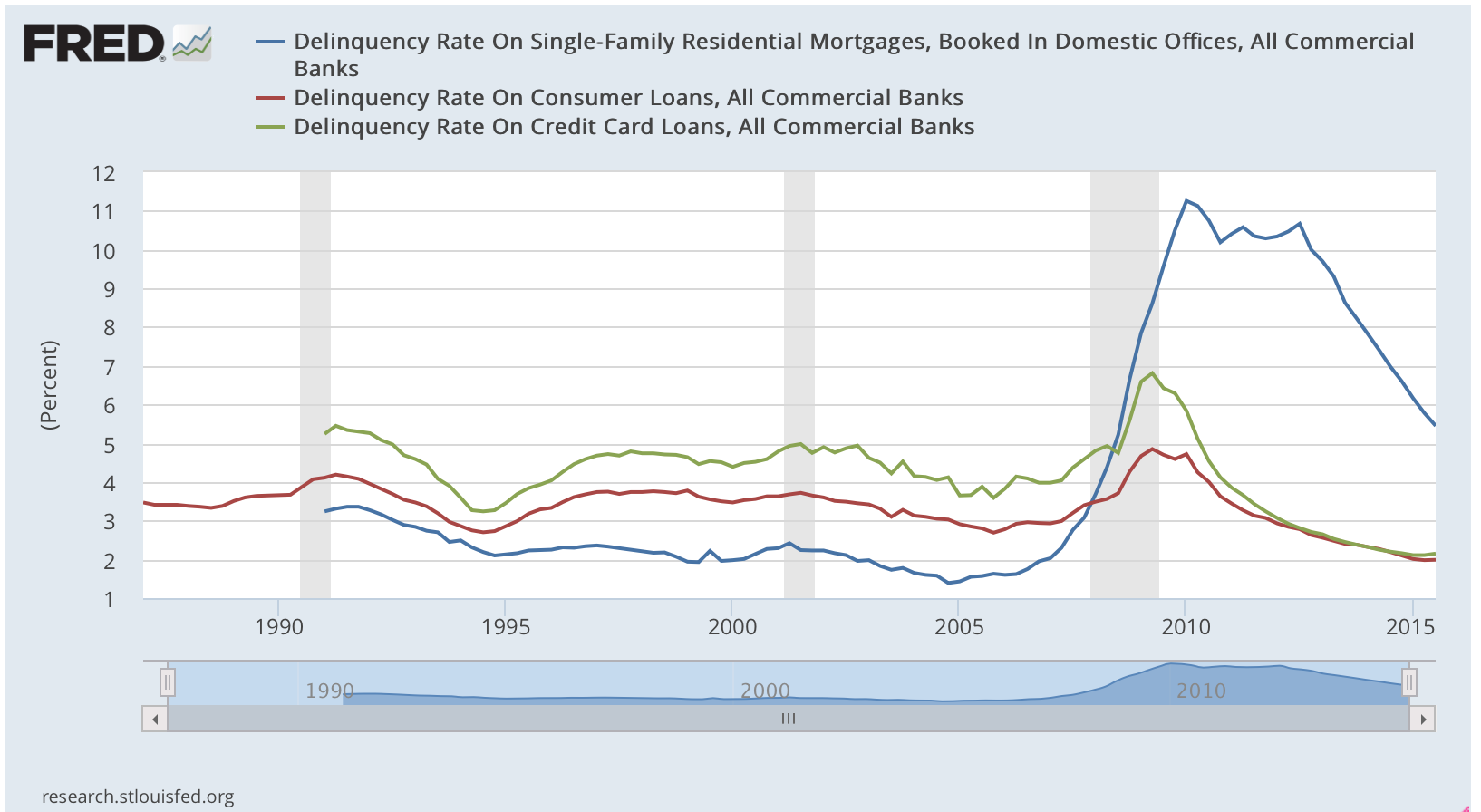

A quick on-line check of some relevant data finds the accompanying graph (click to enlarge). While delinquency rates on these consumer loans differ from the number (or the percentage) of flesh-and-blood Americans who are having trouble paying their bills, these delinquency rates are difficult to square with Akerlof’s and Shiller’s claim that “most” Americans are having significant trouble paying their bills.