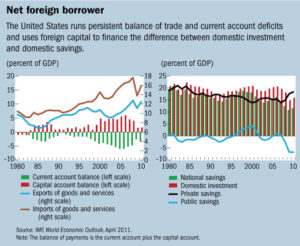

It’s routine for a country’s current-account deficit (or, more loosely, “trade deficit”) to be described as a macroeconomic phenomenon, one that reflects a shortfall of domestic savings. Here’s a typical example:

This highly common manner of framing a trade deficit is highly misleading. This framing springs from an accounting identity: if, during some time period, the amount of investment that occurs in a country exceeds the amount of savings by the citizens of that country, this difference is reflected in the excess of the value of that country’s imports over the value of its exports.

Here’s a simple example. Suppose it turns out that in 2017 Americans bought $1 trillion of imports but sold only $600 billion of exports. What did foreigners do with the remaining $400 billion that they didn’t spend on American exports? Why, they – by definition (and, largely also in practice) – invested those dollars in the American economy. The American economy, therefore, had in 2017 $400 billion more invested in it than was supplied by Americans.

The standard conclusion drawn from this fact is that Americans saved too little (in this example, $400 billion too little). It is also frequently said that, in a situation such as this, that we Americans had to rely upon foreigners to “finance” our current-account deficit.

This framing of trade deficits is done by free traders no less than by protectionists. As I said, it’s a very common way of describing trade deficits. Indeed, it’s the standard framing.

Free traders often use this framing to argue against protectionist policies designed to reduce trade deficits. Free traders, correctly opposing such policies, typically (but I think wrongly) say something like “Our trade deficit is a macroeconomic phenomenon. It reflects our unwillingness to save all that must be saved in order to finance our investments. Given that we want to invest (say) $900 billion but save only $500 billion, the remaining $400 billion must be drawn in from foreigners.”

The mistaken assumption here is that we – the domestic citizens – are the exclusive drivers of all the investments made in our country. We want to invest in these enterprises, in those ventures, and in that set of business expansions. But we have insufficient domestic savings to use to finance these investments that we are undertaking. So, alas, we must get the additional financing from foreigners.

Wrong. Wrong. Wrong. In practice at least some, maybe most – and in principle possibly all – investments made domestically might be driven by foreigners. Investments made domestically are often the ideas of foreigners and are taken under, and driven by, foreigners’ initiatives. Such foreign investments made domestically would not otherwise be made had not some foreigners the entrepreneurial ideas and gumption to make these investments. And so if foreigners also finance, out of their own savings, such investments made in our country, it is an error to regard these investments as “our desired” investments that we nevertheless fail to save enough to finance.

Put differently, the fact that such investments made in the domestic economy are financed by foreigners is not the result of foreigners coming to our rescue to supply financing for some of “our” investments that we’re to spendthrift to save enough to finance ourselves. Rather, such investments are ones that would not occur without foreigners’ initiative. Nor would these investments necessarily be financed by us if only we’d saved more.

In short, it is deeply misleading to point to foreign financing of what, in our economy, I’ll call “foreign-initiated investments” as evidence of deficient domestic savings. This framing is misleading even though foreign financing of foreign-initiated investments do indeed put upward pressure on the domestic trade deficit (or, if “we” had a trade surplus, downward pressure on “our” trade surplus).

Here’s a simple example. Suppose that the CEO of Ikea, impressed both by Americans’ high income and by the relative security of property and contract rights in the United States, chooses to build 50 more retail stores throughout the U.S. Let’s say that the total value of the resources required to build and initially stock these 50 stores is $2.5 billion. And let’s say that all of the $2.5 billion comes out of the savings of Swedes and other non-Americans. This $2.5 billion investment swells the U.S. current-account deficit by $2.5 billion.

But in what way can it meaningfully or usefully be said that this increase in America’s current-account deficit reflects an additional $2.5 billion deficiency in Americans’ savings? None. Had Ikea chosen not to build these additional 50 stores in the U.S., these investments would not have occurred. Nor is it the case that Ikea would have preferred the financing of these stores to come from Americans but, when no Americans came forward with financing, bit the bullet and found the financing elsewhere.

Instead, these investments increased the stock of capital goods in use in the American economy by $2.5 billion. And no Americans (except, perhaps, some furniture retailers) are any poorer as a result. No American (again, except, perhaps, some furniture retailers) necessarily has a diminished stock of assets. (Americans who sell the land to Ikea on which Ikea’s store will be built might all use the proceeds of these sales to increase the value of their bundles of assets in ways that do nothing directly or necessarily to decrease America’s trade deficit – say, by starting new firms in America, by expanding existing firms in America, or by buying equity shares in American corporations.) And no American is made more indebted as a result of this investment in America by Ikea.

Bottom line: Once we recognize that the size of the capital stock is not fixed, and that it can be expanded domestically by foreigners with entrepreneurial ideas applied in the domestic economy, the notion that financing (whether debt or equity) supplied by foreigners necessarily reflects a deficiency of domestic savings is revealed as mistaken. It follows that a current-account (or trade) deficit is not usefully described as the difference between domestic savings and investment – a difference caused by “macroeconomic” forces.

Epilogue: Nothing said above denies the reality that if domestic citizens save more the current-account deficit might fall and that this fall in the size of the current-account deficit might be good for the domestic economy. But it remains untrue both that a current-account deficit necessarily reflects a genuine deficiency of domestic savings, and that a fall in the current-account deficit is necessarily beneficial to the domestic economy.